Despite the recovery in the shares, our system continues to identify a number of accounting flags at aberdeen group. Foremost amongst these is the ‘accrued income’ balance, which has continued to rise from what we already flagged as a high level in 2023. Since this balance is only disclosed once per year in the annual report, we haven’t been able to update our thesis until the publication of the 2024 annual report this week.

As explained in our previous note, accrued income arises when fee income is recognized but where the amount has not yet been billed to the customer. Because asset management has a short billing cycle (monthly or quarterly), it’s unusual to see large balances of accrued income build up. This raises the question of whether aberdeen has been aggressive with revenue recognition by recognizing revenue early and ‘parking it’ on the balance sheet. As KPMG mentioned in their audit report last year “the nature and complexity of management fee calculations has increased year on year”. That complexity can create opportunity.

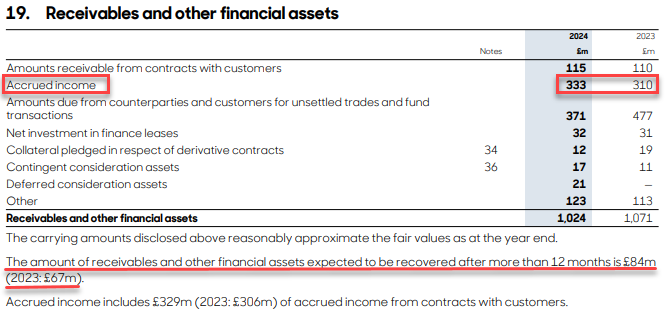

The extract from the 2024 annual report below shows accrued income rising from £310m to £333m, an increase of 7%. What’s concerning about this is that it has risen in a year where management and performance fees have declined by 11%. The value on the balance sheet of £333m now compares to management and performance fees in 2024 of £815m. That’s equivalent to nearly 5 months of fees.

Over the past 4 years in fact, we’ve seen accrued income rise every year even as fee income has declined every year. Our updated chart below shows fees falling from £1.3bn in 2021 to £815m while accrued income has risen from £260m to £329m.

Note also the disclosure below the table (underlined in red) that the ‘amount of receivables and other financial assets expected to be recovered after more than 12 months is £84m”. This amount has grown from just £34m in FY22. This begs the question of why such a high proportion of these receivables won’t be paid out in the next 12 months (again, consider that asset management normally has a very short billing cycle).

As mentioned previously, aberdeen is under great pressure to demonstrate a successful turnaround, by stabilizing revenues while reducing costs. At the same time the company has experienced a huge amount of management churn, with three different CFOs over the past 18 months. Investors should be aware that this kind of pressure, combined with turnover of management can create an even more fertile environment for accounting problems to arise.

Our machine intelligence helps Portfolio Managers to spot critical red flags hidden deep within the financial statements and governance disclosures.

Forensic Alpha uses proprietary machine intelligence to identify risks hidden deep within the financial statements and governance disclosures.

Forensic Alpha Limited

Level 39, One Canada Square

Canary Wharf

London E14 5AB

Forensic Alpha US INC

12 East 49th Street

New York

NY 10017

USA