We first drew attention to growing risks at First Solar in July last year, following the publication of the Q2 filing. Our note highlighted the growing level of finished goods inventory in the context of faltering demand and production that was running close to nameplate capacity. We recommended investors to continue tracking the inventory level closely.

With the Q1 filing published on Tuesday, we find that our panel of flags continues to flash red for this company (now generating a score of ‘10’). This includes DSO, DSI, “Inventory breakdown: and ‘Accounting Policies”

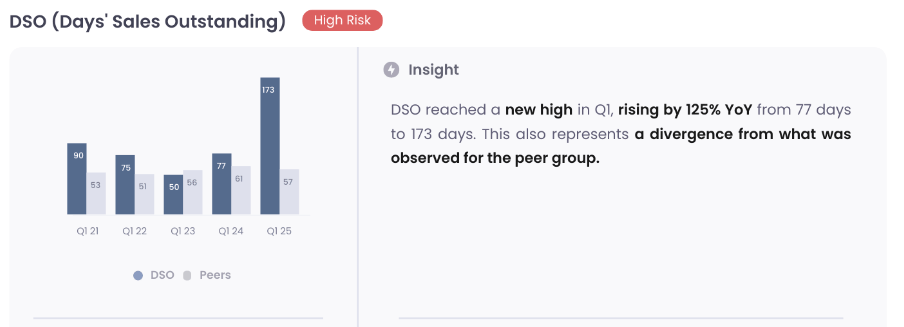

DSO saw a particularly sharp rise as accounts receivable on the balance sheet exploded in the past 3 months from $1.26bn in Q4 to $1.61bn in Q1. The DSO in Q1 over the past 5 years is shown in our automated chart below:

This unusual increase was raised on the call by the CFO and attributed to an increase in overdue accounts:

“We've seen an increase in our overdue accounts receivable balance of approximately $350 million as of quarter end. Within this is approximately $70 million due from 1.8 gigawatts of terminations primarily due to default in 2024. We've not received the entitled termination payment and are continuing to pursue litigation or arbitration to enforce our full termination payment rights under the respective contracts. In addition, a negotiated settlement with a customer following a payment default has deferred approximately $100 million of payments until Q4 of this year. While this deferred payment is fully backed by a surety bond and carries interest that is accretive to the year, it nevertheless creates an additional near-term liquidity imbalance. We've also seen a recent increase in overdue AR as a function of ongoing discussions with customers related to the initial Series 7 manufacturing issues last year.”

Alexander Bradley, CFO

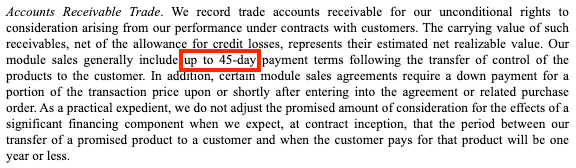

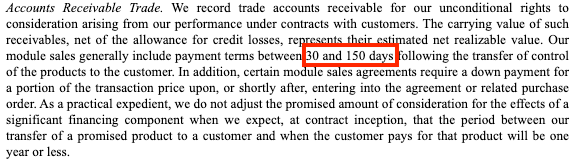

An increase in overdue accounts is concerning in itself, and raises questions about recoverability of these receivables. However we’re not sure this is the full story. Our software drew attention to a small change in the “Accounting Policies” section of the 10-K which is likely to have a big impact. We see from the extracts below that the standard payment terms for modules have changed from “up to 45-days” to “between 30 and 150 days”. This suggests that the company is actively offering extended credit (up to 5 months) to customers as standard. This would certainly manifest as much higher receivables.

Furthermore our software picked up a second important change in the revenue recognition policy. For the first time, in the 2024 10-K filing, the disclosure mentioned the existence of ‘Bill-and-hold’ arrangements, which result in a sale being recognized even where the physical inventory remains in First Solar’s warehouse.

Such ‘bill-and-hold’ arrangements are commonly associated with aggressive revenue recognition, particularly in situations where it is introduced as a new practice. Combined with the previous disclosure indicating extended payment terms, this suggests that the company could be booking sales on modules where neither payment nor delivery is expected in the next 5 months.

This is reminiscent of the scheme run by Al “Chainsaw” Dunlap at Sunbeam, recounted in the book “Financial Shenanigans” (see extract below).

“Sunbeam, anxious to boost sales in its “turnaround year”, hoped to convince retailers to buy grills nearly six months before they were needed. In exchange for major discounts and longer payment terms, retailers agreed to purchase merchandise that they would not physically receive until months later. In the meantime, the goods would be shipped out of the grill factory in Missouri to third-party warehouses leased by Sunbeam, where they would be held until the customers requested them”.

Financial Shenanigans 4th Edition, Howard M. Schilit

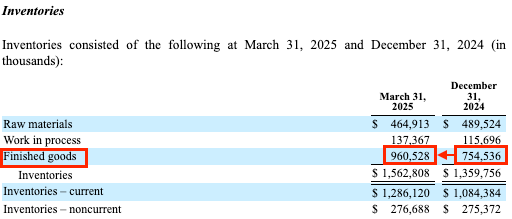

Since inventory held under ‘bill-and-hold’ arrangements is considered sold, it will not appear on First Solar’s balance sheet. This makes it all the more alarming that inventory levels on the balance sheet continue to rise nonetheless. As seen below, finished goods inventory increased by 27% in just 3 months. This comes on top of the 42% increase in 2024.

Based on the current level of COGS, this inventory represents nearly 6 months’ worth of sales (excluding any amounts under bill-and-hold). On the Q1 call, the CFO explained that demand in the second half was likely to absorb some of this excess inventory.

“...our 2025 shipment profile, with its back-ended revenue profile, assumes continuous production throughout the year to meet our contracted commitments. This profile results in a transitory working capital imbalance leading to an increase in our finished goods inventory and warehousing costs, thereby creating near-term headwinds to our gross cash. Pending any potential impact to international production as a function of the new tariff regime, which I'll discuss shortly in the guidance section, we expect this trend to continue in the near term, but anticipate it will reverse once our shipments increase in the second half of the year, reducing our inventory build.”

Alexander Bradley, CFO

However it is worth remembering that finished goods inventory was already coming off an elevated level at the end of 2024. Indeed management commented on this elevated level on the Q4 call, blaming the ‘back-end loading’ in 2024.

“we are finding ourselves right now storing significant volume of product in inventory because of the back-end loading that we saw in 2024, some of the shipment delays that we saw at the end of '24 as a function of customers looking to move things around and associated with the warranty issue that we talked about.”

Alexander Bradley, CFO

An added layer of complexity is created because of the imposition of US tariffs on countries where First Solar has factories: 26%, 24% and 46% applicable to India, Malaysia and Vietnam, respectively. The company does not provide us a breakdown of where the finished goods inventory is located, but potentially much of it sits in jurisdictions that will incur import tariffs, potentially leaving this inventory ‘stranded’. Indeed some inventory under bill-and-hold arrangements may even have been ‘sold’ but not yet delivered! Regardless of where tariffs settle or the demand environment, we’re expecting more trouble ahead in the second half as these balance sheet issues start to manifest.

Our machine intelligence helps Portfolio Managers to spot critical red flags hidden deep within the financial statements and governance disclosures.

Forensic Alpha uses proprietary machine intelligence to identify risks hidden deep within the financial statements and governance disclosures.

Forensic Alpha Limited

Level 39, One Canada Square

Canary Wharf

London E14 5AB

Forensic Alpha US INC

12 East 49th Street

New York

NY 10017

USA