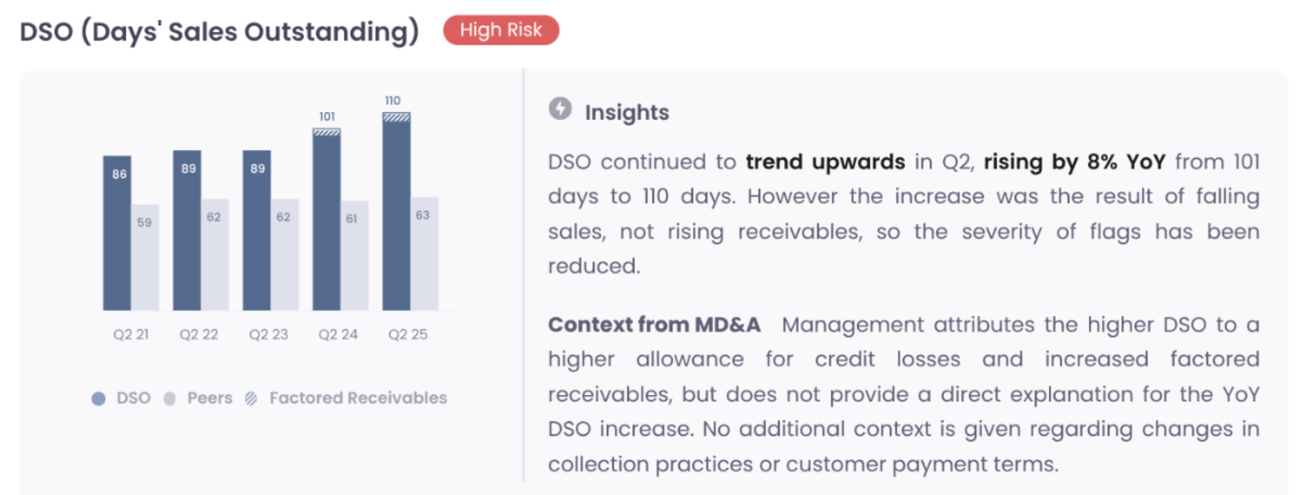

Genpact saw a number of new flags with the publication of the 10-Q filing this week, mostly related to the growth of certain line items on the asset side. Key among these was DSO, which continues to trend upwards

Following another jump in receivables in Q2, DSO now stands at 110 days as shown in the extract from our report below (after adding back factored receivables). While it may simply reflect weaker collection, rising DSO can also be a sign of aggressive revenue recognition. This is a particularly acute risk for services contracts where billing is often on a ‘time and material’ basis, creating scope to inflate invoices or play with the timing around raising an invoice.

Perhaps more concerning than the rise in DSO, is the increase in “Deferred Billings” and “Contract Assets”. These balances reflect revenue recognized on contracts where the customer has not yet been billed. Increasing balances are often associated with aggressive revenue recognition.

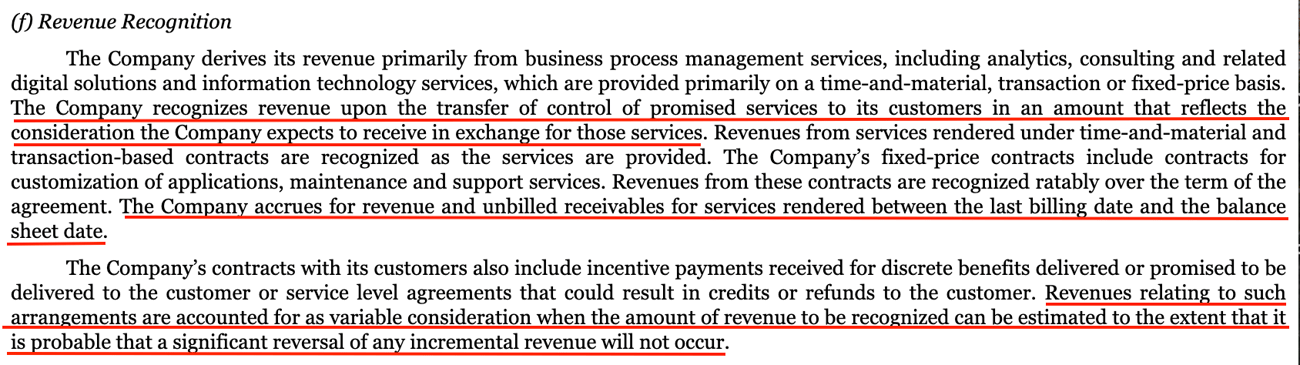

The accounting policy section sets out the conditions under which these are recognized. The extract from the 10-K below indicates that revenue is recognized “upon transfer of control of promised services to its customers in an amount that reflects the consideration the Company expects to receive in exchange for those services”. Thus, there is a degree of estimation involved in the process.

The policy goes on to explain that the contracts may include a variable element: “incentive payments received for discrete beneifts delivered or promised to be delivered to the customer or service level agreements that could result in credits or refunds to the customer”. This heightens the risk that revenues might be overstated. As the policy states: “Revenue relating to such arrangements are accounted for as variable consideration when the amount of revenue to be recognized can be estimated to the extent that it is probable that a significant reversal of any incremental revenue will not occur”. The determination of what is “probable” will be made by the company itself (albeit reviewed by the auditor).

Deferred Billings is the larger amount, and disclosure in the Q2 filing shows that it increased sharply in the first half, from $123m at year end, to $180m (a massive 46% rise). Note that this was on top of an existing increase in 2024 (from $86m to $123m). In the context of a company that generated operating income of $179m in Q2, this balance has suddenly become important. However there is little mention of it, either by management or from the sell side.

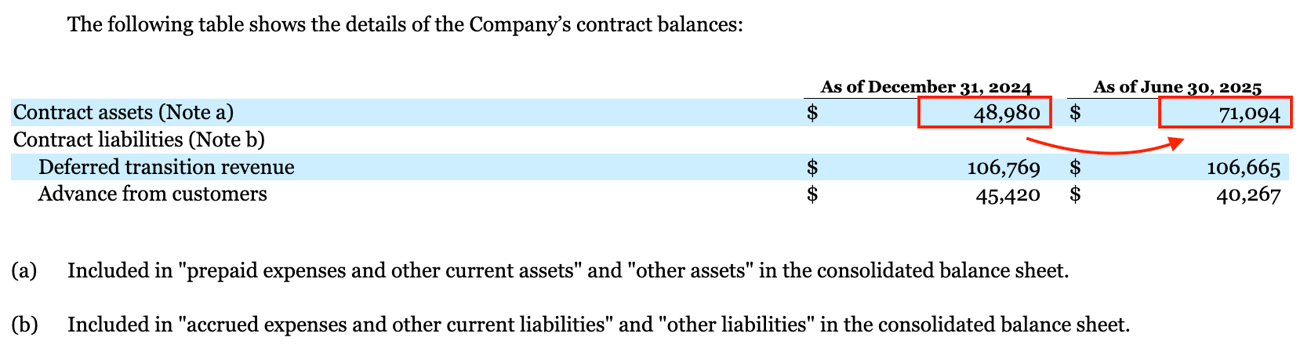

In addition to deferred billings, the company also has growing contract assets. As seen in the extract from the 10-Q below, contract assets grew from $49m to $71m in the last 6 months (a 45% rise). What’s more 40% of these assets are now classified as “non-current”, which is up from 33% at the start of the year). This suggests that revenue is being recognized on contracts where the cash is not due in the next 12 months.

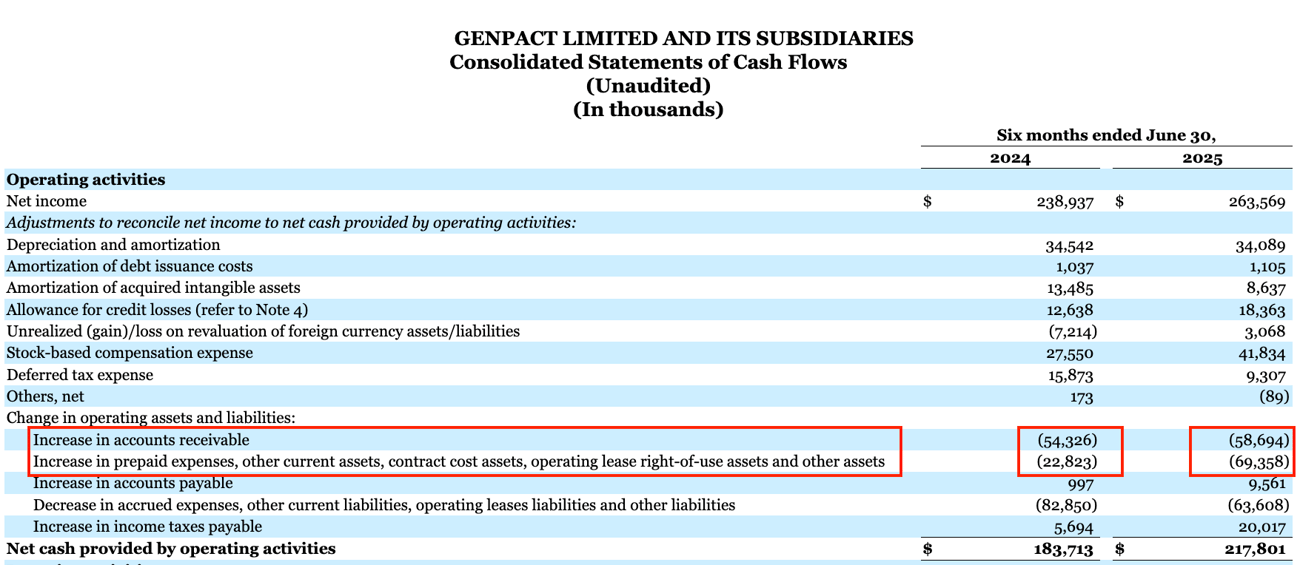

This divergence between revenue recognized and cash flow is one of the key reasons why operating cash flow has lagged operating earnings. This is illustrated neatly by the cash flow statement for H1, showing the material impact of growth in these line items (see extract from 10-Q filing below).

Perhaps to compensate for the underlying weakness in cash flow, the company has been ramping up its factoring program. Disclosure in the notes to the 10-Q tells us they have 2 factoring programs, as set out below:

The first program is a revolving accounts receivable facility of $60m.Over the course of the last 6 months, the use of this facility increased from $26.6m to $59.9m (i.e. close to the maximum). The increase in the first program is significant and would have represented a benefit to cash flow of around $33m in H1.

The second program is a factoring facility covering the company’s largest clients. In Q2, Genpact sold $74.5m of receivables, broadly stable versus previous quarters. As per the disclosure, use of this facility has been at its maximum since 2024.

Revenue recognition is a highly important factor in driving the income statement, and particularly so for a professional services company. Recognizing revenue early or recognizing bogus revenue inflates the top line, but it also has an outsized impact on earnings since the cost base is not inflated to the same degree. Disclosure of executive incentives in the proxy filing highlight a company which is highly focused on revenue growth - 45% of the CEO’s bonus payment and 50% of the long-term PSUs are linked to revenue - much higher than the average for the peer group.

We also note the auditor is KPMG in Mumbai, and they have been in place now for over 20 years. While Genpact does have its roots in India, it is incorporated in Bermuda, it listed on the NYSE in 2007 and its head office, including the finance function, is in New York. This makes it a somewhat unusual set up and raises questions around the effectiveness and independence of the audit process.

The combination of skewed incentives and sharp movements in accruals over the past 6 months warrant particular caution, we believe. While the market is almost exclusively focused on the trajectory of revenue growth and margin in 2025, we are inclined to pay far more attention to the balance sheet and cash flow instead.

Our machine intelligence helps Portfolio Managers to spot critical red flags hidden deep within the financial statements and governance disclosures.

Forensic Alpha uses proprietary machine intelligence to identify risks hidden deep within the financial statements and governance disclosures.

Forensic Alpha Limited

Level 39, One Canada Square

Canary Wharf

London E14 5AB

Forensic Alpha US INC

12 East 49th Street

New York

NY 10017

USA