Softcat originally came onto our radar back in 2022, due to a sharp increase in DSO. Trade receivables had increased by 66% in FY22, and DSO stood at 159 days. At the time, the company explained this was due to a “transient expansion in year-end trade receivables” as a result of implementing a new finance system in Q4 24.

However, since then receivables have not come down. More than 2 years later we can see from the chart below (extracted from our automated report) that DSO remains elevated, and has even crept higher. With the publication of the half-year numbers this week, DSO now stands at 166 days.

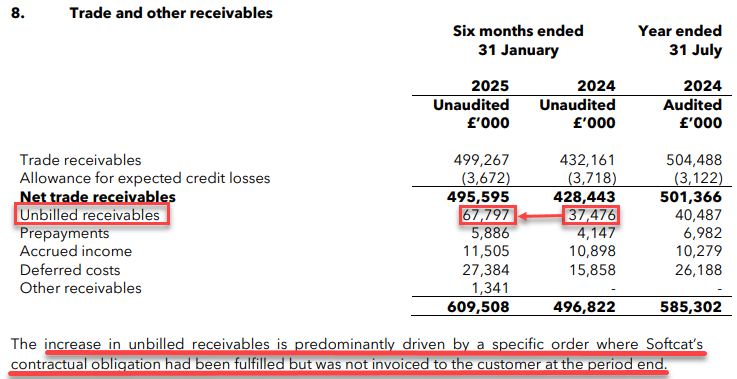

Furthermore, our system has now picked up another red flag associated with “unbilled receivables”, which has suddenly grown by over 80% YoY, from £37m to £68m (see extract below). Unbilled receivables represent amounts already recognized as revenues but not yet billed to the client. Because recognition involves a degree of judgement, sharp increases are often associated with aggressive revenue recognition.

Note also the footnote below the table explaining that the increase was “predominantly driven by a specific order where Softcat’s contractual obligation had been fulfilled but was not invoiced to the customer at the period end.” This suggests there was one particularly large customer where the sale was booked just ahead of the period end even though there was no invoice. We are also left wondering why the customer was not invoiced before the period end even through the contractual obligations were fulfilled.

Assuming all of the increase in unbilled receivables was down to this order and assuming a gross margin in line with the group as a whole, if the order hadn’t been booked we calculate the gross profit for H1 (£220m) would have been lower by around £11m. Instead of reporting 12% growth in gross profit and surprising the market on the upside, that growth would only have been 6%.

The simultaneous growth of both trade receivables and unbilled receivables raises a concern around aggressive revenue recognition. We find it unusual in a sector like this, where the cash cycle should be reasonably short, that there are such high levels of receivables.

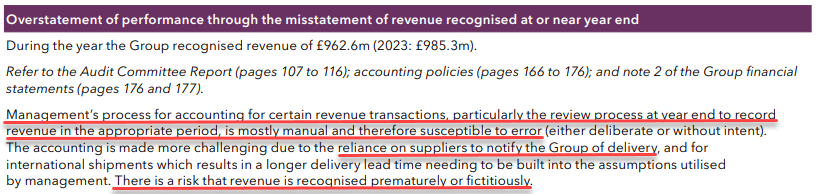

These flags are particularly concerning because of the manual process that the company uses to make adjustments to revenue at the period end. The auditor, EY, raises this in their report as a ‘key audit matter” (see extract below from the FY24 annual report). The report states that the system is ‘susceptible to error’ and relies on notifications from suppliers. They conclude that “there is a risk that revenue is recognised prematurely or fictitiously”. Investors should note that H1 numbers are particularly susceptible to error since they are not subject to an audit.

Our machine intelligence helps Portfolio Managers to spot critical red flags hidden deep within the financial statements and governance disclosures.

Forensic Alpha uses proprietary machine intelligence to identify risks hidden deep within the financial statements and governance disclosures.

Forensic Alpha Limited

Level 39, One Canada Square

Canary Wharf

London E14 5AB

Forensic Alpha US INC

12 East 49th Street

New York

NY 10017

USA