Stora Enso delivered a somewhat lacklustre set of full year results, as increasing fiber costs held back profitability. However, one bright spot was the impressive reduction in working capital, helping to drive strong operating cash flow and reduce gearing.

The chart on the left here shows net debt to adjusted EBITDA moving back from a peak of 4.0x to 3.0x, towards the target of < 2.0x. Meanwhile Operating Working Capital (“OWC”) has dropped to a record 7% of sales.

This achievement was celebrated on the earnings call, by the CFO, Niclas Rosenlew:

"When it comes to our operating working capital, we saw a clear improvement throughout the year. This was thanks to dedicated and focused actions. And the working capital ended at a record low EUR 544 million in the fourth quarter. This was actually a reduction of more than EUR 700 million since the peak some 1.5 years ago. The operating working capital to sales was 7% in Q4, actually a record low, down from 14% at the peak."

The annual report was published two days after this earnings call and provided much more precise information about the changes in working capital, which were picked up by our automated system. One revealing disclosure in the notes shows the rapid growth in the use of factoring arrangements (see extract below). This shows a substantial increase in receivables derecognized, from EUR 178m to EUR 414m. The increase of EUR 236m represents over 80% of the EUR 283m working capital improvement achieved in 2024.

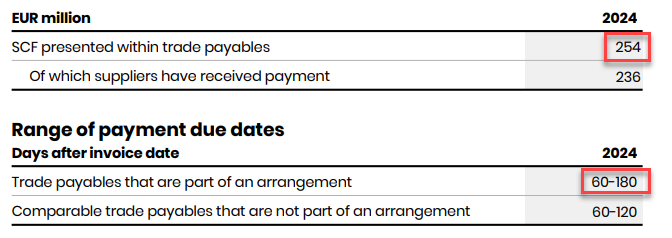

Furthermore, for the first time, there was disclosure of a supplier finance program. These are programs where a financial institution steps in to make payment to suppliers in lieu of the company (usually allowing earlier payment to suppliers). The company then becomes liable to the financial institution, with payment terms which are normally extended relative to standard terms. These payables remain part of the company’s trade payables, so are excluded from net debt. We can see from the disclosure extract below that there were EUR 254m of payables outstanding under the program at the year end. These payables generally had longer payment terms that extended to 6 months. This was likely a large part of the reason for the increase in trade payables of EUR 115m in 2024, another key driver of working capital improvements.

Taking this all together, it is likely that absent the factoring and supply finance program, working capital would have increased, not decreased in 2024. It would seem then that the “dedicated and focused” actions taken by management revolved mostly around financial engineering rather than operational improvements. Without the support of these programs,

e would have seen a materially different trajectory for cash flow, net debt and gearing. As an illustrative example, if there had been no improvement in working capital, net debt would have been 4.0bn (rather than 3.7bn) and gearing would have risen to 3.3x (rather than 3.0)

Our machine intelligence helps Portfolio Managers to spot critical red flags hidden deep within the financial statements and governance disclosures.

Forensic Alpha uses proprietary machine intelligence to identify risks hidden deep within the financial statements and governance disclosures.

Forensic Alpha Limited

Level 39, One Canada Square

Canary Wharf

London E14 5AB

Forensic Alpha US INC

12 East 49th Street

New York

NY 10017

USA