Through divestments and targeted acquisitions Trimble’s pitch is that they are becoming a “Simplified and Focused Organization”. A reader of the 10-K might disagree with this.

From an accounting perspective, Trimble has not had a good start to the year. The filing of the 10-K was delayed by nearly 2 months due to hold-ups in the audit process. When it was published, it came with an adverse opinion from the auditors on the company’s internal controls over financial reporting (an issue that dated back to the 2023 filing). Just 4 days later, the company dismissed the auditor (EY). Despite this, the share price has been remarkably resilient.

It is in this context that we saw our risk rating rise sharply from a ‘5’ to a ‘10’. We have identified a number of issues from the 10-K (for FY24) and now the 10-Q (for Q1 25), which was published on Monday this week. The flags cover two key areas - capitalization of costs and the risk associated with equity investments, each covered in turn below:

The key flag from the 10-K was the capitalization of sales commissions (listed in the 10-K as ‘Deferred Costs to Obtain Customer Contracts’). Disclosure in the notes tells us that the balance of this item rose by nearly 30% in 2024, from $96.4m to $124.3m (see extract below). The disclosure also tells us that this balance is included within the line item “Other non-current assets”

A second disclosure tells us that they are capitalizing ‘cloud computing arrangements’, with the balance increasing by 10% from $58m to $64m (see extract from the 10-K below). Note that while the associated amortization expense has risen sharply, this is explicitly excluded from the company’s definition of “adjusted EBITDA”. Although they were previously capitalizing cloud computing arrangements, this was the first time there was explicit mention of it in the accounting policies section (perhaps one of the sources of friction with EY?). This balance is included in both “Other non-current assets” and “Prepaid expenses”.

Taking the two line items identified above (“Other non-current assets” and “Prepaid expenses”), we have tracked their development over time in the table below. This shows these line items have grown in 2024, and continue to grow in Q1 25.

The growth was particularly significant in 2024 (+$91m), obscured by the fact that a large balance of non-current assets were classified as ‘held for sale’ (and subsequently disposed of with the mobility divestiture). The remaining accounts continued to grow in the first quarter, up by $25m. This raises questions about whether there are other expenses (beyond the two specified above) which may have been capitalized here.

As existing investors will know, divestitures have been a key part of Trimble’s strategy to streamline the organization. In Q2 2024, Trimble disposed of its Ag business into a JV jointly owned with AGCO (PTx Trimble). Then, in Q1 2025, they sold the Mobility business to Platform Science, taking a 32.5% stake in Platform Science in the process.

While these entities have been deconsolidated from the balance sheet, Trimble continues to have significant economic exposure. This exposure is reflected in the growing balance of “Equity Investments”, which has grown from $128m at the end of 2023, to $619m at the end of Q1 25. This includes $220m for the 15% stake in PTx Trimble and $254m for the 32.5% stake in Platform Science.

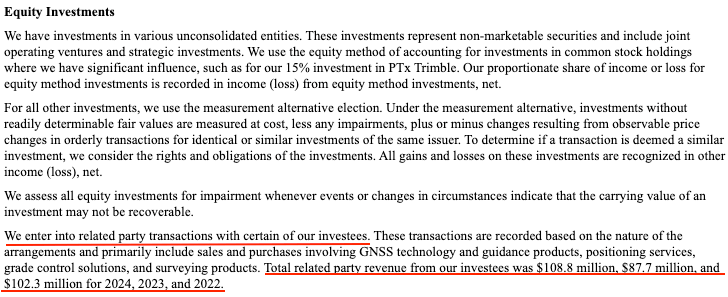

In addition to the investment, we see from the disclosure (extract from the 10-K below) that they continue to derive significant revenue from their equity investments, amounting to $109m in 2024. We believe a large part of this likely relates to the 7 year supply agreement to provide GNSS and guidance technologies to PTx Trimble (2024 disclosure would presumably reflect 9 months of this revenue).

This matters because the performance of the Ag business seems to have dramatically declined since the sale was agreed. During the year ended December 31, 2024, AGCO recognized an impairment charge of $351m on a goodwill balance of $1.6bn - due to a deterioration in the near-term outlook driven by ‘weak industry demand and lower market penetration’.

Looking into the disclosure from AGCO’s 10-K (extract below), since PTx was consolidated it has contributed a loss of $350.9m to AGCO (representing 9 months since 1st April 2024). It’s not clear if this includes the impairment charge mentioned above, but either way this represents a sharp decline in profitability since the sale (Note that the Ag business transferred by Trimble was generating operating income of $171m in 2023). It also raises questions about whether the JV might need some form of support from equity holders (including Trimble) in the future.

Divesting non-core businesses has been a key part of the strategy to simplify the organisation. However given the exposure that Trimble still retains via these equity stakes and the losses made in 2024, this doesn’t exactly look like a ‘clean-break’.

Our machine intelligence helps Portfolio Managers to spot critical red flags hidden deep within the financial statements and governance disclosures.

Forensic Alpha uses proprietary machine intelligence to identify risks hidden deep within the financial statements and governance disclosures.

Forensic Alpha Limited

Level 39, One Canada Square

Canary Wharf

London E14 5AB

Forensic Alpha US INC

12 East 49th Street

New York

NY 10017

USA